Geopolitics to the Fore Again

- Geopolitics continues to unnerve markets globally

- US dollar, gold, and the bond market are likely to be the kneejerk assets of choice

- UK MPC sprang a surprise and raised rates by 50bps

- UK longer dated gilts hold in but two year bond yields spike

- European growth tips down and may take the equity market with it

- Hopes that China's Politburo will deliver a fiscal boost in July

The events unfolding in Russia over the past few days have highlighted the fragility of global geopolitics. In what can be termed as one of the most remarkable moments since the Russian invasion of Ukraine began, thousands of mercenaries, led by a rogue leader, threatened to take control of Moscow. Although the rebellion eventually fizzled out, it was nonetheless a grim reminder of what unfolded at Capitol Hill in the United States, where a few hundred protestors stormed the seat of the U.S. government, exposing its vulnerability and demonstrating that nothing was as secure as once thought. While Putin may have gained an upper hand currently, the events have left Russia somewhat destabilised, with the president evidently feeling less secure than before. The markets may hold a glimmer of hope that the events over the weekend will persuade the Russian President to scale back his "special operation" in Ukraine, but this remains uncertain.

Now, to the more mundane aspects of the global financial markets. Investors continue to hope that inflation will eventually lose its teeth. Currently, however, it is continuing to surprise by beating consensus expectations. Last week, UK inflation surprised significantly on the upside, leading the UK Monetary Policy Committee (MPC) to raise rates by an unusually high 50 basis points (bps). While the UK may be viewed as an outlier in this regard, even as it grapples with structural inflationary pressures stemming from the effects of Brexit, it joins the Reserve Bank of Australia and the Bank of Canada in instituting monetary tightening measures that have surprised the markets significantly.

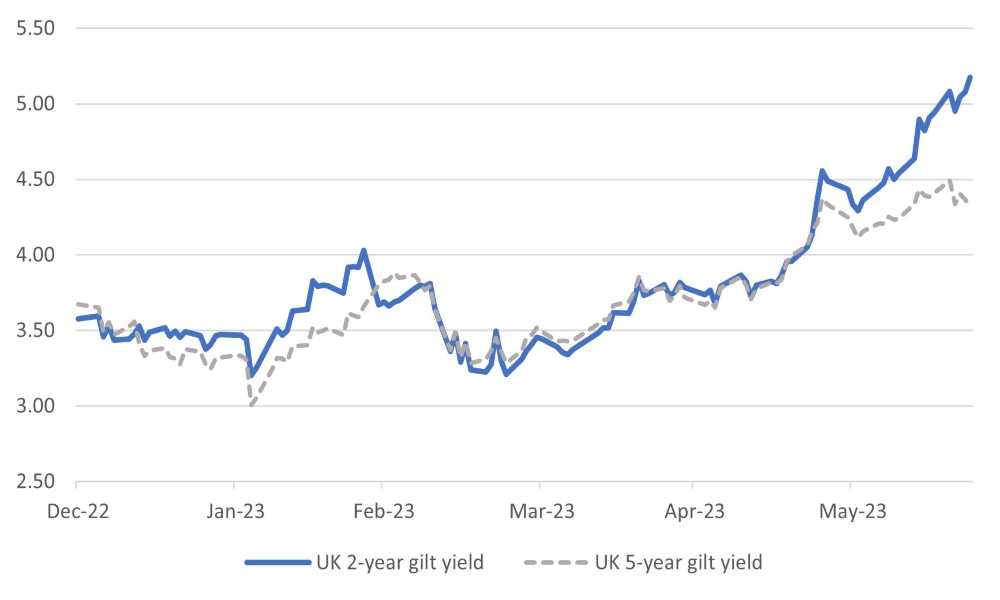

Headline inflation in the UK came in at 8.7%, well above consensus expectations of 8.4%. Of particular concern to the markets was core inflation, which surged to 7.1% from 6.8%, prompting the MPC to vote 7-2 to raise rates by 50 bps instead of the previously signalled 25 bps. Market expectations now point towards UK policy rates peaking at 6.25% by the end of the year, which is an increase of nearly 50 bps from the level anticipated just a week ago. Despite the prospect of higher interest rates, the British pound depreciated against the dollar, declining by a cent to 1.2617. The argument put forth is that elevated interest rates could pose challenges to economic growth and potentially push the UK into a recession, with a peak policy rate of 6.25% risking a 2% decline in UK GDP.

The UK inflation shocker had a negative impact on short-dated gilts, making them the weakest performer of the week, with two-year yields increasing 10 bps to 5.14%, to a level comparable with that of Brazil. However, in what can be seen as preserving the credibility of the monetary authorities, the yield on the UK 10-year bond drifted lower, suggesting that the actions taken by the MPC will have desired effects in the long run.

Chart 1: UK two-year gilt yield rises on poor inflation news, 10-year gilt yield well anchored

Source: Bloomberg

Source: Bloomberg

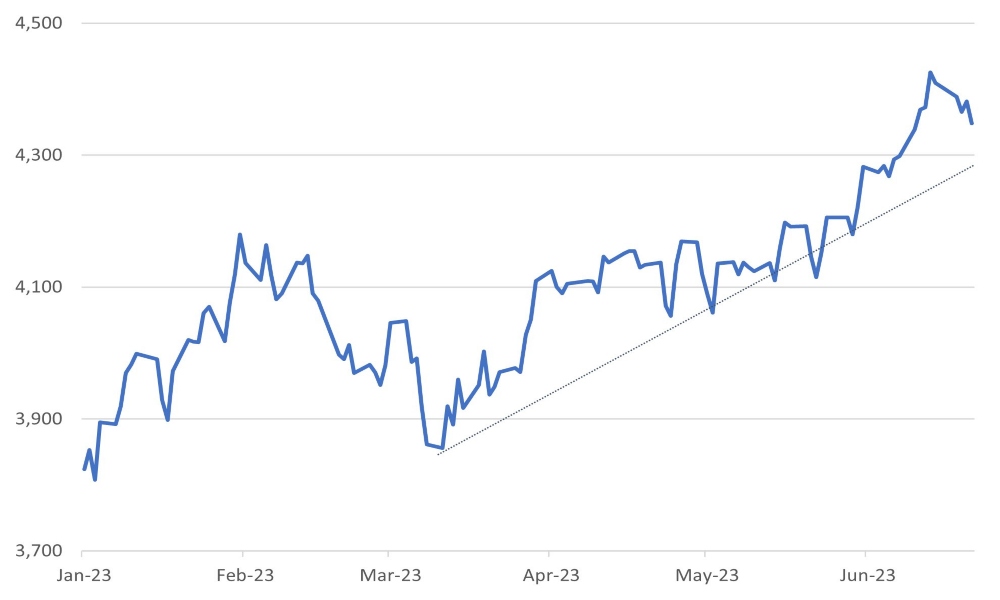

In a broader sense, the financial markets are grappling with growing concerns shared by central banks regarding the pace of economic growth and lingering inflation. Last week, global equities experienced a 2% decline as investors acknowledged the global slowdown in growth in the backdrop of the ongoing inflationary challenges. From a technical standpoint, it is worth noting that the US equity market, represented by the S&P500, would need to decline an additional 3% to breach the current uptrend that has been in place since mid-March. On a technical breakdown, the market could be sliding towards its March lows.

Chart 2: S&P 500 tops out on growth and inflation concerns – 3% downside to key support

Source: Bloomberg

Source: Bloomberg

European economy tips down and may take the equity market with it.

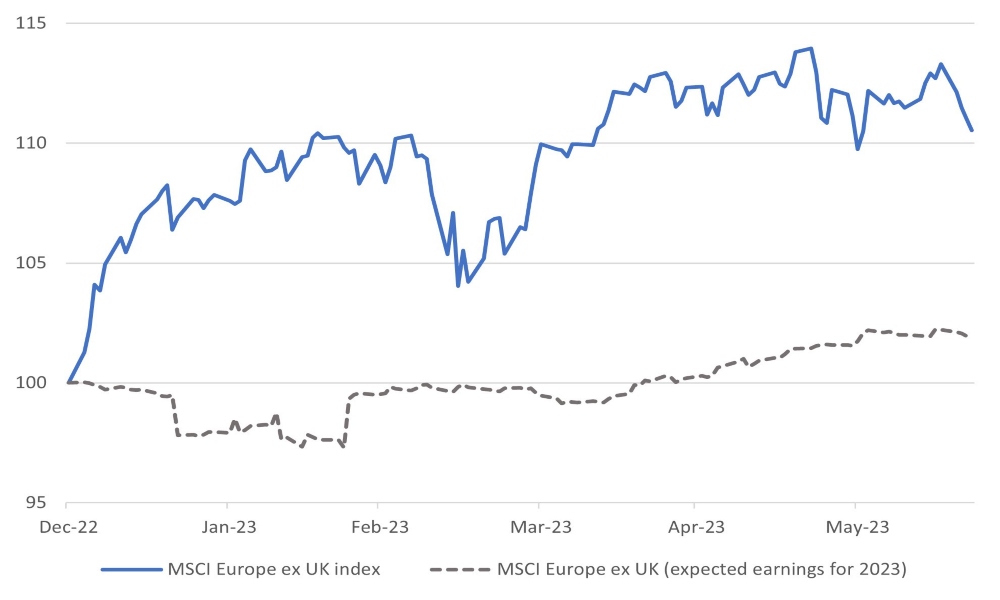

Market concerns regarding growth are particularly focused on Europe, as indicated by last week's array of economic data pointing to a loss of momentum. The composite Purchasing Managers' Index (PMI) for the eurozone declined to 52.8 in June from 50.3 in May, reflecting a continued drop. The weakness remains concentrated in the manufacturing sector, with the PMI falling to 44.1 from 46.4. The services sector PMI also showed signs of weakness, declining to 52.4 from 55.1, but remaining above the crucial 50.0 level, indicating that the sector is still expanding.

There is a silver lining in the data, however, as it provides evidence of abating inflationary pressures, albeit at a faster rate in the manufacturing sector compared with services.

The European equity market has moved sideward in recent months as the global focus has been on technology and the US equity market. It’s difficult to see much near-term performance given the headwind of further ECB rate rises and the prospect of some downside to corporate earnings forecasts given the loss of growth momentum.

Chart 3: European equity markets may start to reflect the fact that corporate earnings forecasts have downside risk

Source: Bloomberg

Source: Bloomberg

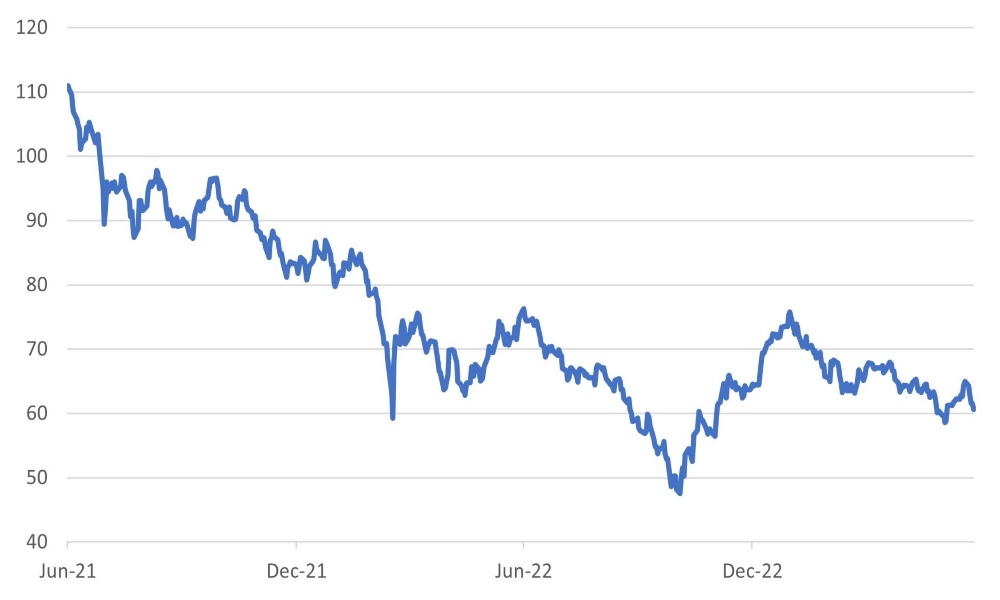

China needs the Politburo to deliver a fiscal stimulus at the July meeting

As we approach the July Politburo meeting, China watchers will be hoping for a more meaningful stimulus to the economy than we saw last week from the central bank. Many an investor is waiting on the Chinese authorities to adjust policy to provide a more significant boost to growth. Last week’s official rate cut and subsequent 10bps cut in the 1-year and 5-year loan rates were seen as adjustments to policy as opposed to a structural shift to easing. Many economists now don’t believe we will see any major shifts of policy until the Politburo meeting in late July. Commentary from the government on the policy shift has been in short supply of late as some of the recent Politburo meetings (most recently May) have had no readout of what was discussed. The July meeting is seen by analysts as key as it probably reflects on the performance of the economy for the half year and should lend itself to decision making.

Chart 4: MSCI China has lost around half of its gains from the lows of 2022  Source: Bloomberg

Source: Bloomberg

Copyright © Dalma Capital, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.