History is not on the Side of a Fed Rate Cut

History is not on the Side of a Fed Rate Cut

- A Federal Reserve rate cut requires a marked deterioration in the US economy and/or a financial crisis

- Chinese equity market needs a revival of consumption, and so does the government

History says a Fed rate cut is not on the cards

Looking back at the history of the circumstances that led to a cut in rates by the Fed, it is evident that an interest rate cut is not on the cards. Of course, a catastrophic fall in the markets or the economy could make the Fed rethink its plans. Table 1 below shows the economic circumstances over the past 40 years that preceded a rate cut after a peak in the tightening cycle. We would make a few observations here:

- Only once (during COVID) did the Fed cut rates when they were negative in real terms – as they are today.

- Unemployment would need to surge to at least 4.0% or, more likely, 5.0% to justify a cut in rates.

- Monthly nonfarm payrolls on a rolling basis would need to fall by at least 100,000, or more to rein in wage inflation.

- A peak in rates has typically occurred with a recession and/or a financial crisis.

- The Fed has never cut interest rates from anything lower than a positive real rate of 1.9%; today, real rates are negative.

We rule out a Fed rate cut unless one or more of the following conditions occur:

- US inflation falls to 3% or lower, and the unemployment rate jumps to 4.5%.

- Global growth collapses

- Financial markets witness a sharp pullback

- A peak in rates has typically occurred with a recession and/or a financial crisis.

- The financial system witnesses a significant stress

Table 1: Trend in five-day change in US 10-year bond yield

| Date | NFP at the time | NFP 1-year averag | U* rate | Fed funds | Inflation | Real Fed funds | Comment |

|---|---|---|---|---|---|---|---|

| Current | 236,000 | 345,000 | 3.5% | 5.00% | 6.0% | -1.0% | |

| 30/04/2019 | 243,000 | 178,000 | 3.9% | 2.50% | 2.0% | +0.5% | COVID related |

| 31/7/2007 | -30,000 | 127,000 | 4.5% | 5.25% | 2.4% | +1.85% | Global Financial Crisis |

| 30/12/2000 | 152,000 | 161,000 | 3.9% | 5.50% | 3.4% | +2.1% | Market collapse |

| 30/9/1998 | 213,000 | 264,000 | 4.5% | 5.50% | 1.5% | +4.0% | Inflation below target |

| 31/5/1995 | -20,000 | 260,000 | 5.5% | 6.00% | 3.2% | +2.8% | Very weak growth |

| 30/9/1990 | -97,000 | 96,000 | 5.7% | 8.25% | 6.2% | +2.05% | Recession |

| 31/5/1989 | 122,000 | 246,000 | 5.2% | 9.75% | 5.4% | +4.35% | |

| 31/8/1986 | 115,000 | 146,000 | 7.2% | 7.25% | 1.6% | +5.65% | Inflation below target |

Source: Bloomberg

China is different

Data due out this week will make it evidently clear that the Chinese economy is at a very different trajectory in its economic cycle relative to much of the rest of the world. While much of the world is struggling to suppress inflation, data from China should show March inflation at a meagre 1.1% year-on-year. We believe the low inflation will make it easier for further central bank and government action to support the economy. We expect China’s central bank, the PBOC, to cut its one-year policy rate by 10bps in due course. We also expect China's new aggregate social financing growth to continue at close to 10% per annum. The data released in March showed that money supply growth in China was running at the fastest pace in some seven years. M2 money supply growth is running at 12.9% year-on-year.

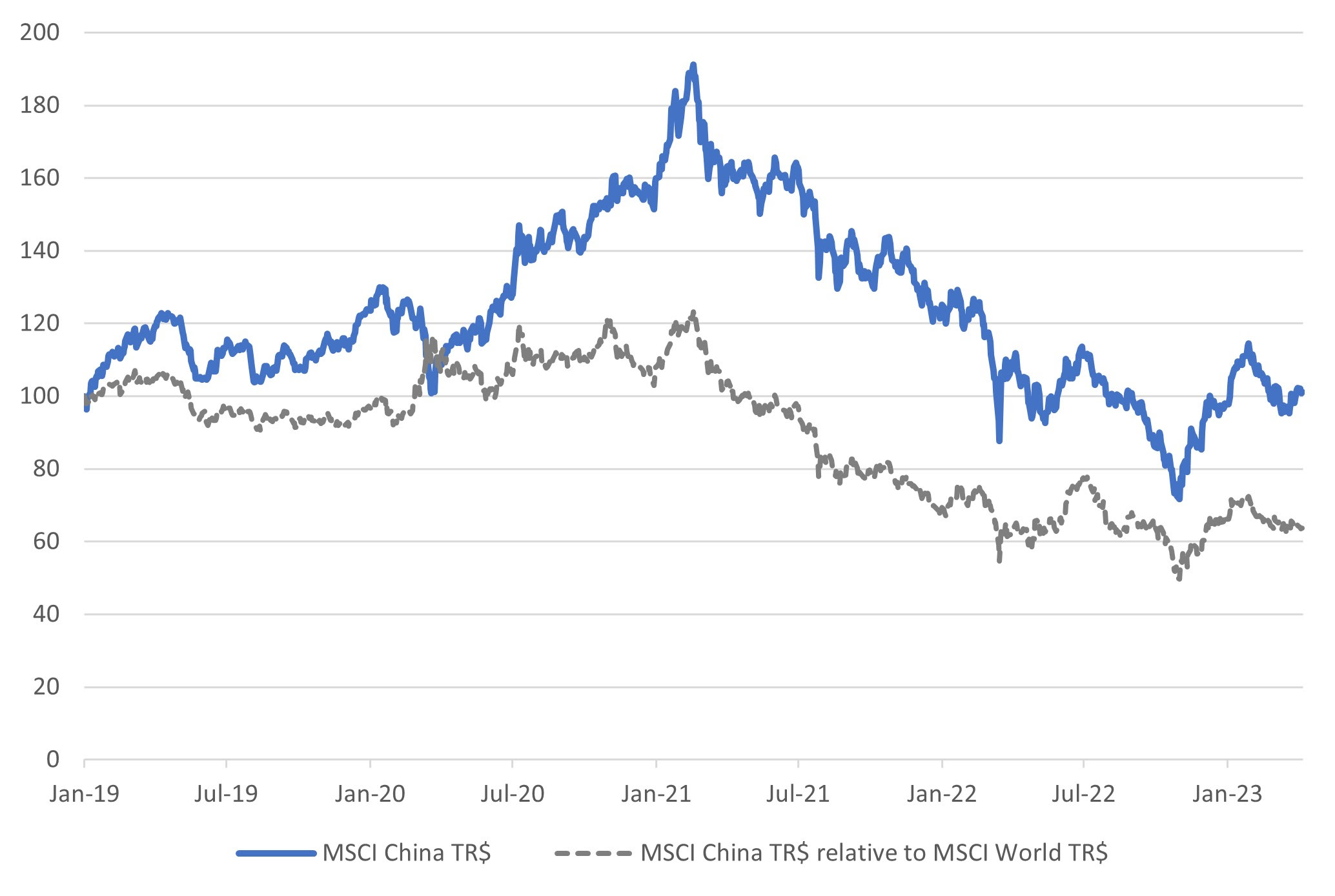

After staging a sharp rebound earlier, the Chinese equity market has lost momentum in both absolute and price-relative terms over recent months. Part of the Chinese market's underperformance has been driven by developed markets benefitting more substantially from the changing market perception about the likely future path of US interest rates.

We advise investors to be patient at this juncture. The market has value, as evidenced by the P/E of the equity market, which is below long-term averages, and the price-to-book value. We must bear in mind that China witnessed stringent lockdowns over a rather protracted period of time. Any economy would take time – and efforts – to recover from such a severe lockdown. Consumers and businesses are only just getting used to their freedom. Moreover, there are some promising signs, with the service sector and construction activity already showing good growth. The consumer sector will be critical, too. Economists expect the Chinese population to eventually catch up on some of the profound underspending seen through the lockdown. China's population has been nervous about spending. A recent PBOC survey, for example, showed that the percentage of residents inclined to "spend more" increased by just 0.5% on the previous quarter to 23.2%. Notable was the weak recovery of car sales in the year to date.

Source: Bloomberg

The challenge about Chinese consumer spending is not the lack of savings or income but more a lack of confidence. We therefore expect the Chinese government to refrain from instituting significant measures to boost income. Household savings rose to 38% of disposable income during the pandemic, the highest since 2014. Damien Ma and Houze Song, writing in Foreign Affairs (China's Consumption Conundrum, March 16th, 2023) highlight the need for the Chinese government to adopt policies that have a structural impact on consumer confidence. These measures include:

- Support for the real estate sector.

- Reversing some of its big-tech crackdowns, particularly on edu-tech, could boost employment. Youth unemployment stands at 17%.

- Addressing the looming pension and healthcare liabilities that worry households.

- Explicitly committing to a pro-consumption agenda.

The political choice of whether to support consumption is stark as the authors note, "China can either choose a pro-consumption path or risk forfeiting its goal of becoming the world's largest economy over the next decade".

As a final note, a survey on Chinese consumer preferences conducted by Deloitte in November 2022, before the lockdown ended, made interesting observations. According to the survey, Chinese consumers were more reflective of their spending preferences during the pandemic than they seemed to have been in the past. Householders had reduced their impulse buying, prioritising quality and value, with a bias towards domestic brands. Consumers were less inclined to satiate their material needs and were more interested in their physical and spiritual satisfaction. They continue to embrace innovation. The survey found that consumers increasingly favoured live streaming and instant retail.

Copyright © Dalma Capital, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.