It Doesn't Get Any Better, It Gets Tougher

The Middle East is at the centre of global geopolitics once again – and this time for some very unfortunate reasons. Whether the developments will have a bearing on the financial markets is something that only time will tell, but the profound human suffering that has affected so many lives will certainly affect our collective psyche. Our hopes and prayers are for an eventual de-escalation and the restoration of peace in the region.

Just a few weeks ago the Middle East was the focal point of discussions at the G20 meetings, as global leaders tried to strike a chord on various issues. What also drew the world’s attention was the proposed India-Middle East-Europe Economic Corridor that promised to be a game changer given its potential to renew global integration. As the situation in the Middle East continues to evolve rapidly, this dream of greater regional cooperation and economic development must not be allowed to falter. The connectivity of the Indian subcontinent with the Western world would usher in an era of economic progress, bringing the opportunity for growth and prosperity to many.

Oil could pose problems

In the interim, these turbulent times carry the ominous prospect of elevated oil prices and heightened economic uncertainty. In essence, inflation is being wielded as a weapon, posing a threat to the supply of oil and potentially causing further disruptions to supply chains, notably through the strategically vital Strait of Hormuz.

Should the current hostilities intensify, there is a heightened risk of a substantial surge in oil prices, with some experts even speculating levels of $100-150 per barrel. Of course, the upper end of this range is contingent on a severe disruption to oil shipments via the Strait of Hormuz. At the very least, we anticipate an immediate upward pressure on oil prices resulting from the likely reinstatement of tighter oil sanctions against Iran. It is crucial to note that Iranian oil sales have covertly risen to the tune of 1 million barrels per day, as the United States had previously tolerated increased Iranian oil supply. It is essential to remind our readers here that the United States’ strategic oil reserves are at their lowest in four decades, providing just 17 days' worth of global consumption.

Gold as a hedge?

In this volatile environment, we continue to advocate for a prudent allocation to gold within investment portfolios. Despite challenges from some quarters regarding the relevance of this asset class in portfolios, particularly with the U.S. dollar showing strength and cash generating attractive returns, it is important to remember that the value of cash does not appreciate when geopolitical challenges loom large. Gold serves as a hedge, insuring against unforeseen or immeasurable risks in the market.

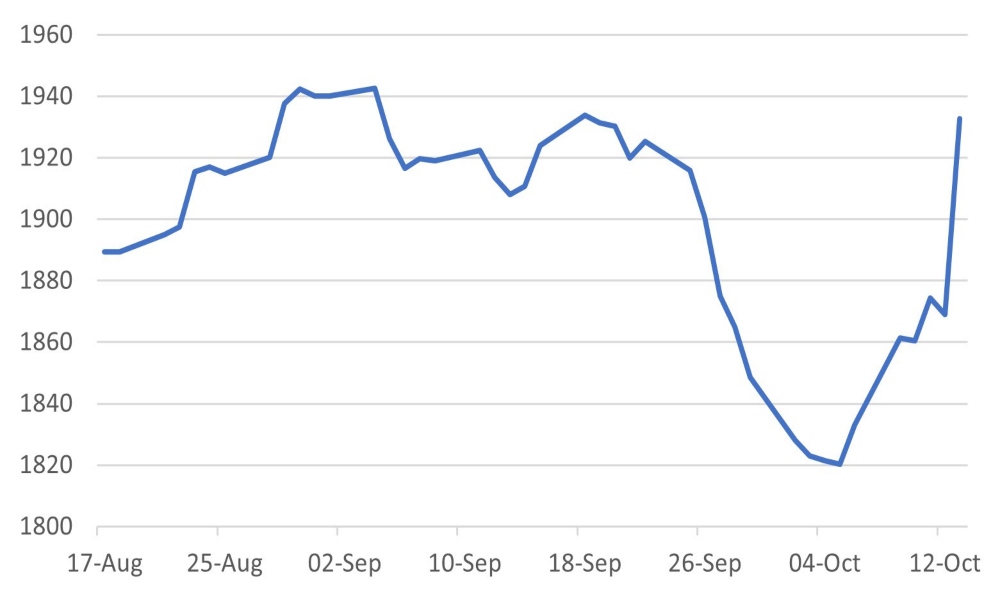

Chart 1: Spot Gold price surges sharply to one-month high from low of $1820

Source: Bloomberg

Source: Bloomberg

Inflation: As troubling as we suspected

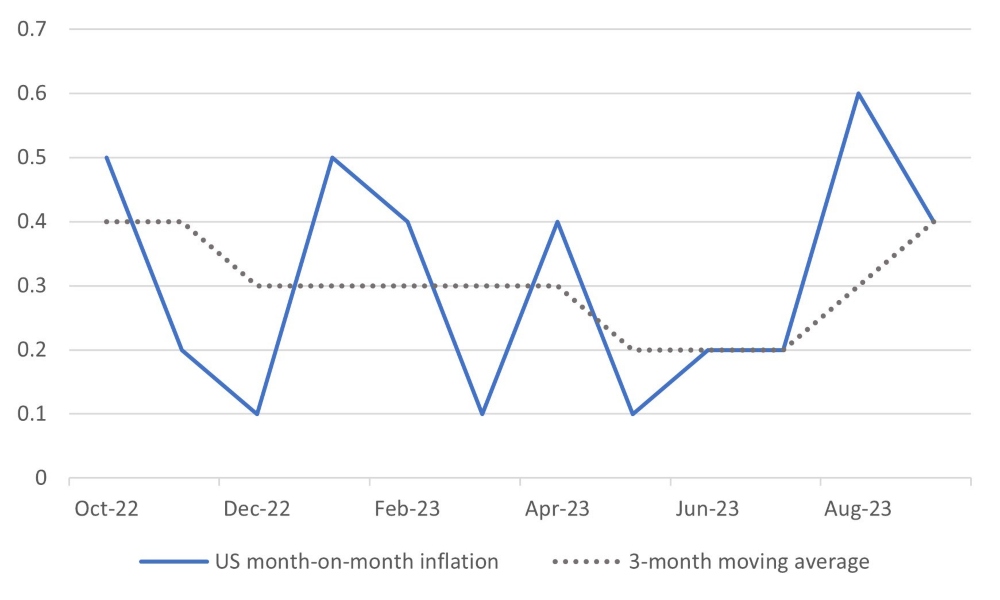

Last week's US inflation report delivered an unexpected surprise to the market, confirming our earlier suspicions. Inflation surged at a higher-than-anticipated 0.4% month-on-month pace in September, compounding the previous month's 0.5% uptick. This current trajectory of greater increase in monthly inflation marks a significant departure from the modest 0.1% to 0.2% upticks observed in the preceding two months.

Last week, markets briefly toyed with the idea that the Federal Reserve might reconsider any further rate hikes. However, by the week's end, the economic data flow demonstrated a reinvigorated inflationary momentum. Both the Producer Price Index and Consumer Price Index surpassed expectations, and the looming spectre of elevated energy prices threatened to exacerbate inflation further.

Chart 2: Month-on-month US inflation re-accelerates

Source: Bloomberg

Source: Bloomberg

It is important to regard the recent market movements and 'expert' opinions on the outlook for US policy rates from last week, as transient noise rather than robust, well-founded analyses. The market's earlier predictions regarding inflation proved inaccurate on many occasions, despite ample pre-data indicators suggesting an upward risk.

Furthermore, some commentators contended that the recent surge in long-term interest rates could obviate the need for further short-term rate increases. Nevertheless, we believe it would be imprudent for the Fed to rely on market-driven interest rate hikes to shape its monetary policy. Substantial academic research supports the notion that it is the central bank's policy rates that wield the most influence in the realm of monetary policy.

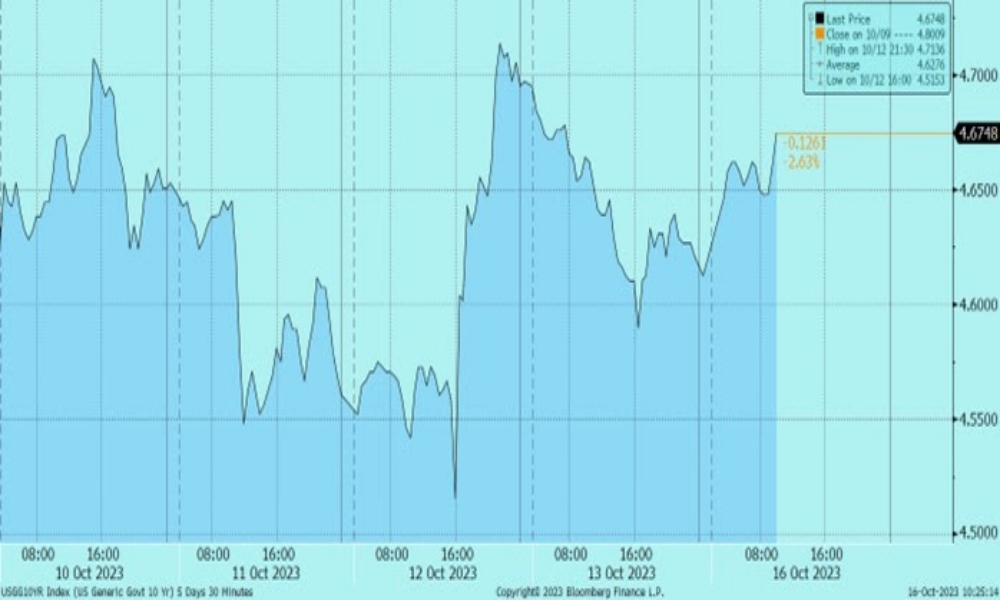

As illustrated in Chart 3, the US 10-year yields fluctuated dramatically during intraday trading. We wonder if investors genuinely believe that a sharp ascent in these market rates alone would be sufficient to compel the Fed to alter its policy stance!

Chart 3: US 10-year intra-day displays significant volatility

Source: Bloomberg

Source: Bloomberg

Peering into 2024 with the IMF

The most recent IMF projections for 2024 make for a sobering read. While they have not shifted significantly from the previous report, the fact that we are a mere two-and-a half months away from 2024 compels us to assess the impending challenges facing the world economy. Global growth is undergoing a noticeable shift, with the developed world showing signs of weakening. Consequently, the global economy is becoming increasingly reliant on emerging countries for economic vitality.

The IMF anticipates a gradual decline in global inflation from its peak of 8.7% to 6.9% by end-2023 and 5.8% in 2024. However, it is worth noting here that IMF has revised its inflation projection for 2024, increasing it by 0.6%.

Here's a summary of the IMF forecasts:

| Region | 2022 | 2023E | 2024E |

|---|---|---|---|

| Global | 3.5% | 3.0% | 2.9% |

| Advanced | 2.6% | 1.5% | 1.4% |

| US | 2.1% | 2.1% | 1.5% |

| Euro Area | 3.3% | 0.7% | 1.2% |

| Japan | 1.0% | 2.0% | 1.0% |

| UK | 4.1% | 0.5% | 0.6% |

| EM and developing | 4.1% | 4.0% | 4.0% |

| China | 3.0% | 5.0% | 4.2% |

| India | 7.2% | 6.3% | 6.3% |

| Saudi Arabia | 8.7% | 0.8% | 4.0% |

Source: IMF

In conjunction with these new forecasts, the IMF commentary underscores the importance of central monetary authorities maintaining credibility in their efforts to restore price stability. Furthermore, it alludes to the critical need for governments, particularly in the United States, to challenge themselves in restoring fiscal discipline.

Cash is King for retail investors?

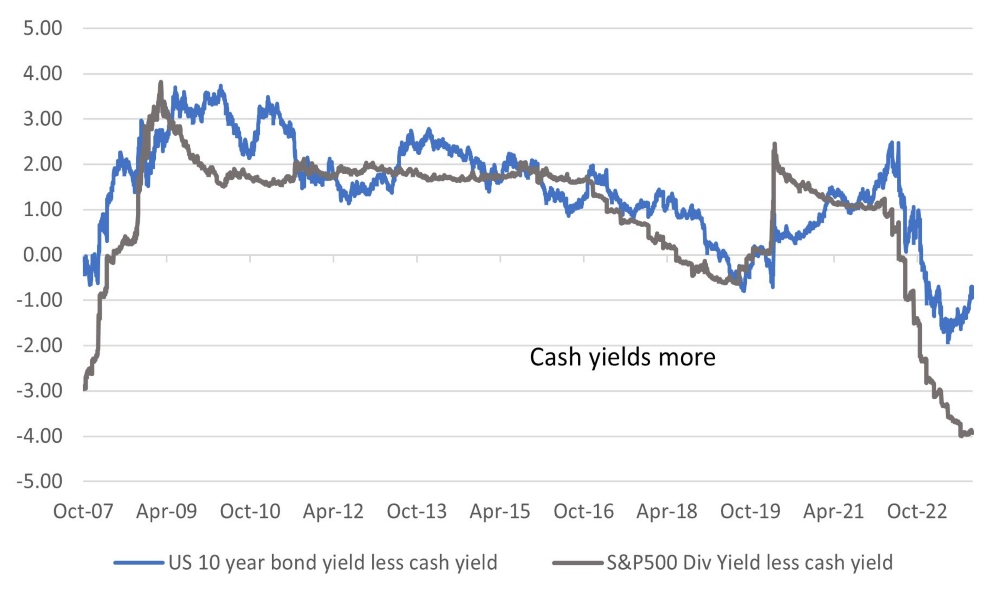

Evidence of retail investors de-risking their wealth came with Blackrock announcing that it had seen a net redemption of $13billion from long-term investment funds, the first outflow since the onset of the COVID-19 pandemic in 2020. While we are sympathetic to investors who are trying to protect their wealth and see the merits of cash yields beating many assets by a good margin, we also believe that when the central bank’s job is done cash yields will fall and bonds will provide the cushion of capital gain from rising bond prices as bond yields fall. A portfolio strategy that has a diversity of bonds and cash is still the right strategy even for this time of higher-than-expected inflation.

Chart 4: US 10-year government bond and US equity market yield less than cash

Source: Bloomberg

Source: Bloomberg

Copyright © The Global CIO Office, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.