It's a Fuzzy World

- The market is split between two distinct views on inflation – higher for longer and heading lower quite soon

- Despite talks of a recession, global growth has surprised to the upside; and modestly, inflation too

- US corporate results so far are much better than (downgraded) expectations

- ETF flows suggest investors making for bonds

- Equity flows are focussed on emerging markets

- We take the non-consensus position to overweight Japanese equities

There’s lot of ambiguity out there. Economists (and the Fed) use the word recession often, but economic activity is not rolling over quite as fast as some had feared. Headline inflation is declining, but core inflation remains persistent. US corporate results are surprising to the upside. Investors, meanwhile, are split into two opposite camps, the worried and the sanguine, with the markets oscillating between the two extreme views.

As investors seek greater clarity in the current environment, they appear to be split down the middle in their views on the future direction that the global economy and the markets will take. It is telling that the hedge fund industry has had a very poor start to the year, with few fund managers being able to earn positive returns in the current volatile environment. The HFRX index of hedge fund returns is up just 0.2% year to date, with many strategies, such as equity long-short and global macro, down significantly.

Two camps

There is a group of investors that expects inflation to persist. This group sees the Fed and other central banks ultimately being forced to raise interest rates and keep them at relatively high levels for an extended period. The other group of investors believes that inflation will be surprising to the downside very soon, and hence the Fed can lift off the brake pedal and cut interest rates through the latter part of the year.

Life is more complex than that. The first quarter economic data has surprised to the upside on both growth and inflation. Last week's US industrial confidence data was surprisingly strong in places, particularly in the service sector. UK inflation, on the other hand, also sprang a significant upside surprise, surging an eye-watering 10.2% year-on-year in March, as food and energy costs remained elevated.

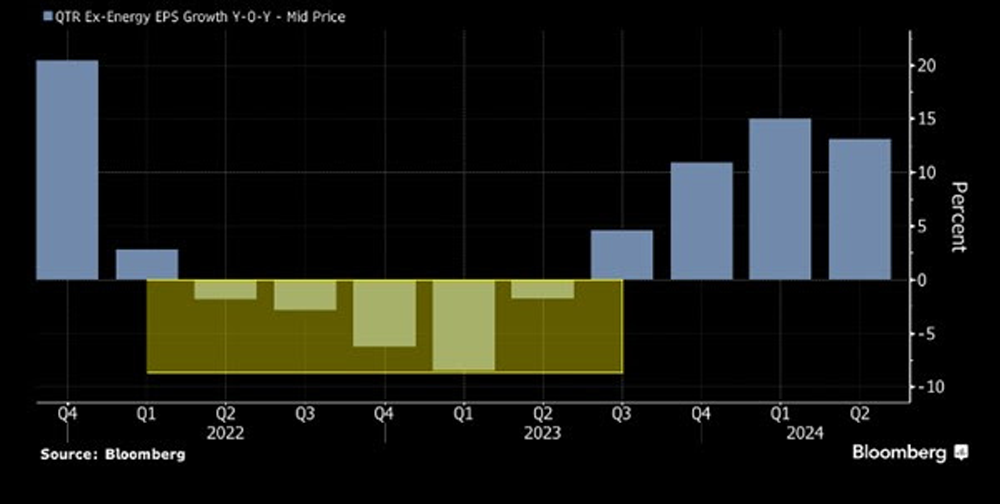

The market’s confusion around trends has spread to the US corporate results season. Ahead of the earnings release, analysts had set their forecasts for a poor outcome as they expected a sharp setback in year-on-year earnings growth. However, a Bloomberg estimates suggests that of the 20% companies that have already reported numbers, more than 77% have posted profits ahead of expectations. It then begs the question as to whether the analysts have been too bearish. Let’s bear in mind that the US corporate results seasons is a quarterly phenomenon where around 65% of the reports ordinarily come in ahead of market expectations…it's just that on this occasion that the percentage of reports beating expectations has been exceptionally high. One might take that trend as bullish for the overall equity market; however, we still believe that analysts are too optimistic about the level of profits for the balance of the year. With even the Fed talking about a "mild recession", it's tough to see how such economic conditions would lead to significant year-on-year increases in corporate profits through the balance of the year and into 2024.

Chart 1: Actual and Expected Corporate Profit Growth for the S&P500 ex-Energy (year-on-year)

Back to 60-40?

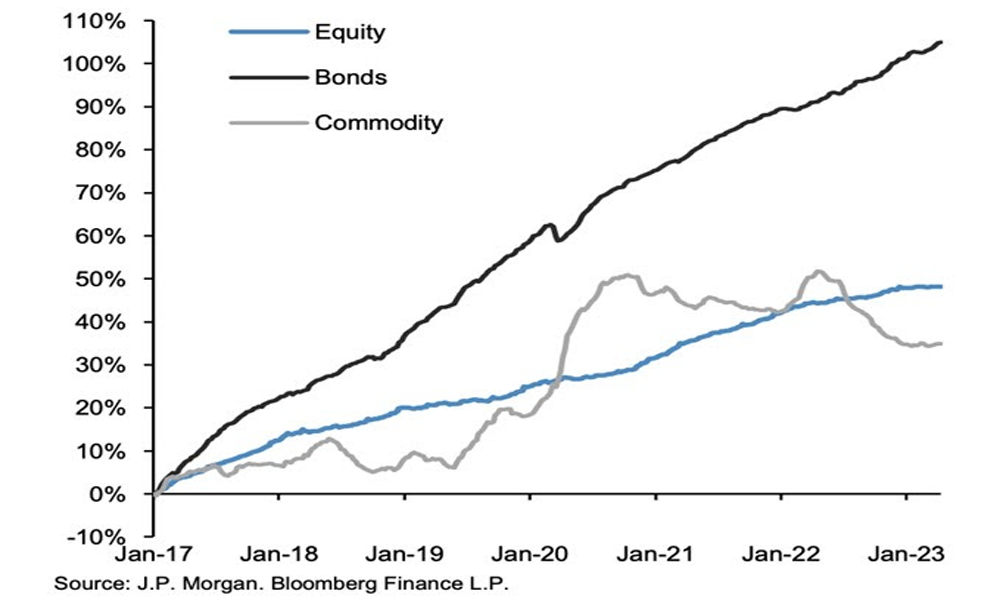

Some data on flows into ETFs for the major asset classes highlights that at the broad asset class level, investors are eyeing an eventual drop in inflation but are wary of the likely decline in growth required to achieve it. Even since 2017, new investments have been focussed on bond ETFs. The flows into bonds have accelerated in the past year (Chart 2). Commentators’ assertion that equities will eventually catch up after their recent dismal performance misses the point that higher interest rates can only encourage an allocation of funds away from equities. While commentators talk about a standard allocation of 60% to equity and 40% to bonds in a portfolio, those numbers moved to 80-20 at the peak of the market's love affair with equities. The last few years' volatile performance of equities and higher yields from cash and bond markets is encouraging a reset of multi-asset portfolios back to their historical 60-40 balance. Hence, it is no surprise to see bond funds seeing a more significant share of ETF inflows relative to the past.

Chart 2: Cumulative Flows into Major Asset Classes

Emerging equities share of global ETFs grows at a good pace

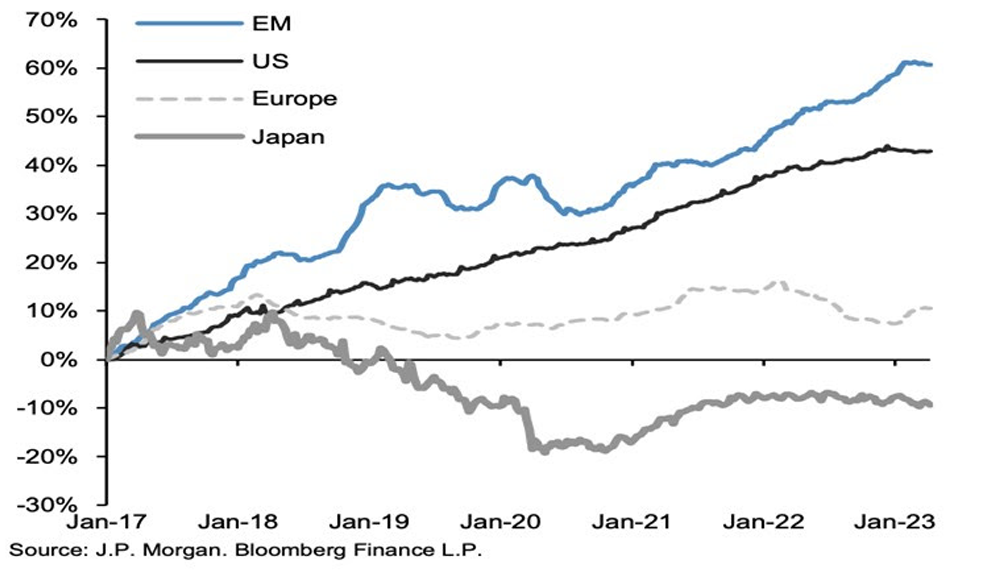

Last week we called for a reallocation of equity portfolios away from the US equity market to emerging markets. Interestingly, the ETF data flow shows that emerging equity markets have been the regional choice for investors' equity allocations outpacing those in the US market.

Chart 3: Emerging Markets Lead Cumulative Flows into Equity sub-Asset Classes

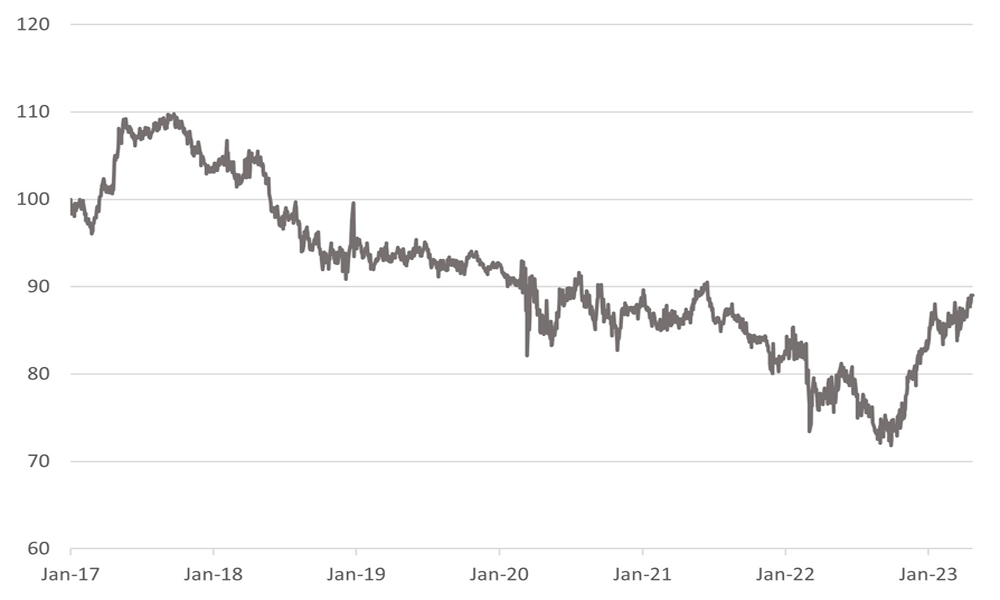

It is noteworthy that ETF investors have missed out on the marked improvement in the relative performance of European equities since mid-2022.

Chart 4: Europe’s Recent Outperformance Versus Global Equities ex-Europe (ex-UK)

Relative rebased to Jan 2017 =100

Source: Bloomberg

In our view, global under-investment in Japanese equities offers a reason to be upbeat about the future relative performance of the market. Several factors are primed to give the market the much-needed support in the future, shaking the deflation mentality that has held back the Japanese economy and its financial markets. This week, investors’ minds will be focussed on the Bank of Japan meeting. While it is a close call, the central bank may not yet be ready to change its monetary policy position. Nevertheless, we still believe that it is only a matter of time before the Japanese central bank abandons its yield curve control and allows long-term interest rates to normalise higher. In our view, the central bank's acceptance of higher bond yields would be a critical factor in generating more of an inflation mentality in corporate and household thinking. More inflation should encourage consumption and investment, reinforcing robust GDP growth.

The corporate sector has already shown signs of reform. Likely record share buybacks this year would be a testimony to the progress in corporate governance improvement underway in corporate Japan. At the start of the year, the Tokyo Stock Exchange announced proposals to put further pressure on listed companies to improve their standards for listing under three headings of Prime, Standard, and Growth. Failure to meet the standards would force the companies to de-list and lose access to equity funding. The essence of the measures is to force companies to improve their returns and be mindful of the cost of capital. Too many Japanese companies trade below their book value because of their poor returns on capital.

According to Lazard Asset Management, the perennially weak Yen leaves the Japanese industry at its most competitive positioning since the 1970s. The competitiveness of the currency leaves it at a rather beneficial position to take advantage of the reshoring of manufacturing and long-term secular trends such as factory automation and vehicle electrification.

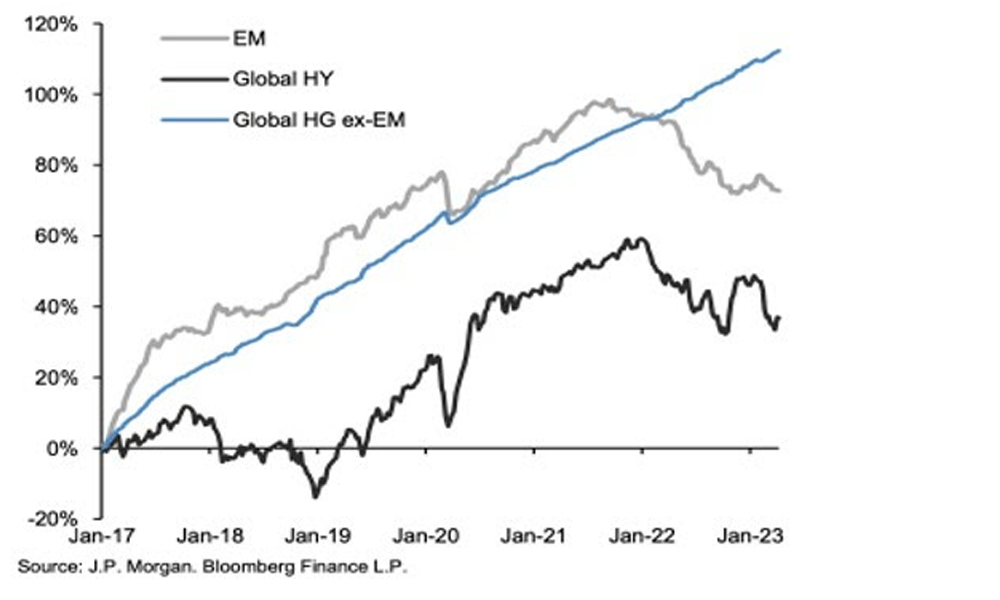

ETF Bond flows lack investor risk-taking

The ETF flows in the bond markets have shown sustained growth in core and spread products such as emerging market bonds and high yield debt. The poor performance of bonds in 2022 sent flows into the higher-risk bonds into the reverse, and they have yet to recover. We have argued before that neither asset class gives enough spread return that outweighs the risks in the global economy. Hence, we remain price-sensitive buyers of both asset classes into any weakness.

Chart 5: Cumulative Flows into Higher Quality Bonds Outstrip Flows into High Yield and Emerging Market Debt

<hr>

Copyright © Dalma Capital, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.