Macro and Markets Monthly

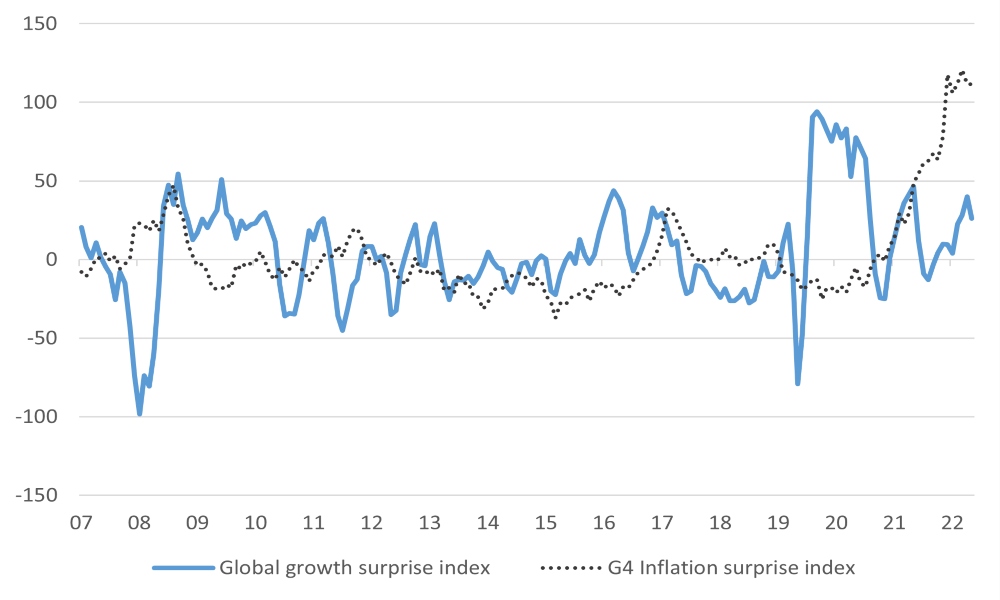

The global economy has continued to generate little more growth than economists had expected and the persistence of inflation. Central bankers remain on watch, with the Federal Reserve still in a mind frame of tightening monetary policy. The economic data has generally come in above expectations, and inflation news has been far more robust than economists had forecasted (chart1)

Growth in Europe and the United States has proved more robust than expected, with the service sector providing most of the momentum. Indeed, industrial confidence surveys show that the manufacturing sector could already be facing a sharp slowdown. However, the service sector has continued to power ahead.

Chart 1: Global economic surprise – inflation and growth

(% yoy)

Source: Bloomberg

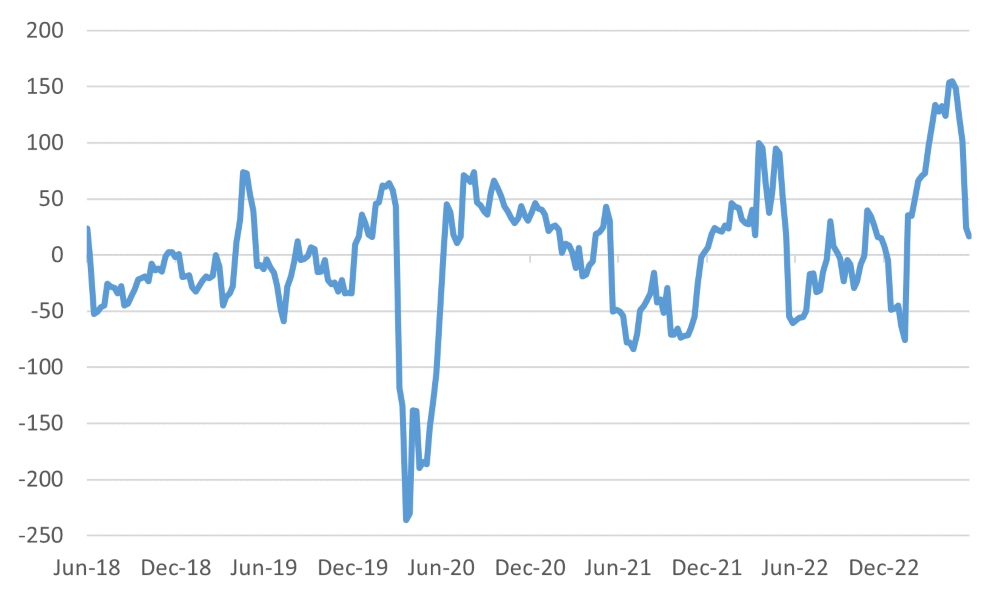

China was the most disappointing economy throughout the month. The economy has not shown the vibrancy that many had expected after the post covid re-opening in January. There has been a slew of disappointing data points in the past month. In particular industrial production growth was at just 5.6% against market expectations of 10.9%. Retail sales and fixed asset investment all came in below expectations.

Chart 2: Economic surprise for China points to loss of momentum

Source: Bloomberg

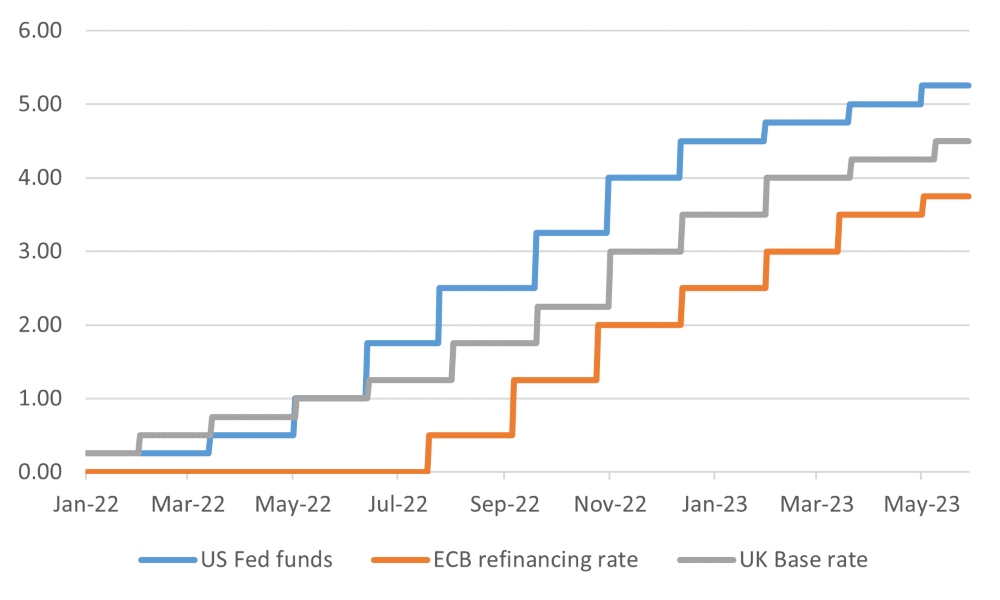

Central bankers continued to raise interest rates. The major central banks will likely have to raise rates further in the coming months. The Federal Reserve, despite giving the impression that they might skip a rate rise at their next meeting, now look likely to raise rates still further at their June meeting after inflation surprised to the upside. The Bank of England has a particular problem as core inflation re-accelerated to 6.8% from 6.2%.

Chart 3: Central Banks continued to raise rates

Source: Bloomberg

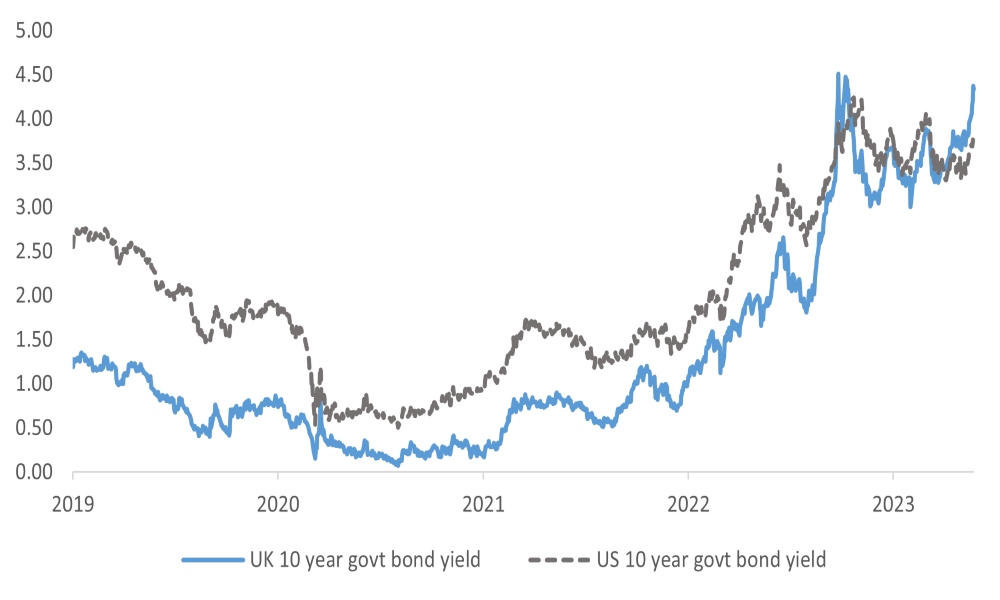

Chart 4: US 10-year bond yield adjusted for inflation

Source: Bloomberg

Markets

Equities

The equity markets had a mixed month ending net down in most markets. Investor worries about a future global recession were exacerbated by the change in economists' views on the peaking of US interest rates weighed on sentiment. By country, Japan was the standout with an excellent month. For the first time in a while, international investor interest is very evident as investors buy-in to the idea that corporate restructuring could be for real on this occasion. The announcement by the Tokyo stock exchange at the beginning of the year that companies would risk being delisted if they didn't improve their governance practices and profitability has had a real impact.

Table 1: Equity Market Returns in May

| US Equities | 0.5% |

| Europe ex UK | -5.2% |

| Japan equities | 6.1% |

| UK equities | -5.4% |

| Switzerland | -1.9% |

| Asia ex Japan | -2.1% |

| Russell 2000 | -1.1% |

| FTSE Small | -1.7% |

| India | 2.5% |

| China | -3.6% |

| Brazil | 3.7% |

| Singapore | -3.4% |

| Emerging markets | -1.9% |

| Developed Market | -1.2% |

Source: Bloomberg

By sector, the standout was the marked appreciation of the tech sector. Indeed, tech stocks accounted for a substantial proportion of the US equity market return. NVIDIA which reported revenues 50% ahead of expectations rose 36% for the month added close to $250 bn to the market capitalisation of the S&P500 equivalent to 70bps of the value of the index. Alphabet, Amazon and Nvidia in aggregate added two percentage points to the value of index.

Table 2: Market returns by sector in May

| Energy | -9.7% |

| IT | 8.0% |

| Consumer staples | -6.8% |

| Healthcare | -4.6% |

| Banks | -5.2% |

Source: Bloomberg

Bonds, like equities, struggled to make any headway in May. The prospect of higher-than-expected inflation for longer and central banks still on a tightening path led to very modest returns at best. Higher spreads for high yield reflected the investor's concerns that a recession could bring a higher risk of defaults.

Table 3: Bond market returns

| Global Aggregate (Hgd) | 0.1% |

| Investment grade bonds | -0.2% |

| Emerging market debt | -0.3% |

| US High Yield | -0.8% |

FX and Precious metals

The dollar recovered some of its poise after the four percent setback in March/April. Clearly, the prospect of higher interest rates helped. The dollar recovered sharply against the Yen up from 132 to 139 over the course of the month.

Gold was relatively unchanged over the course of the month, although having sold off from much higher levels of $2050 to finish the month at $1962.

Table 4: Monthly performance of precious metals and currencies for May

| Gold | -1.0% |

| Silver | -6.0% |

| $ trade weighted | 2.1% |

| GBP trade weighted | 1.5% |

| Yen/$ | -1.3% |

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.