Policy Makers Still Hard at Work

- Fed to leave rates unchanged, but signalling is evident that its job is not done

- ECB raises rates by 25bps and signals rates to stay high for some time

- Government bond yields pushing higher – oil prices a risk

- China gives us some good news but foreign investors show little appetite to invest

The Federal Reserve is unlikely to announce a further rate increase at its Wednesday meeting. However, the release of a fresh round of economic projections from the central bank will shape the mood of the market. We expect the Fed to signal that a further rate hike in the near future cannot be ruled out. Inflation is still well above target, and economic data has suggested that the economy, unlike projections, is in a mini cycle of re-acceleration (Exhibit 1).

Chart 1: US Economic Growth Potentially Re-accelerating

US Economic Surprise Index

Source: Bloomberg

Source: Bloomberg

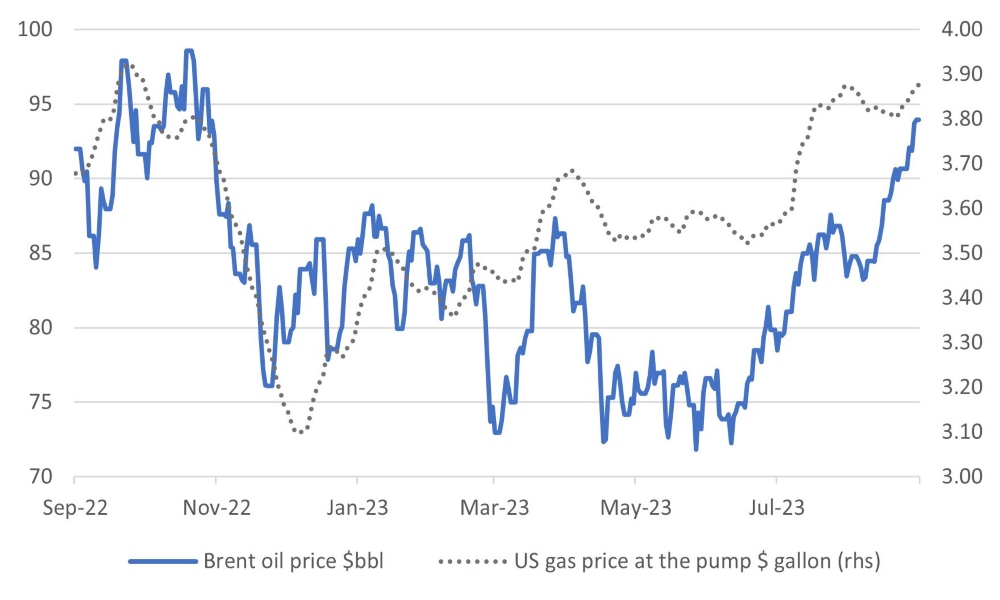

While some rather exuberant market commentators tried to interpret the strength in recent economic data as suggesting that US inflation was losing momentum, the truth remains far from it. As we have suggested repeatedly in recent months, there are significant upside risks to the oil price – and inflation – given the supply constraints and ongoing robust demand. After declining by an annualised 12% rate in the six months to May, global energy prices surged 14% in the three months to August, and there has been no letup in the upward move in prices so far (Exhibit 2).

Chart 2: Oil Price and US Gas Prices Up Sharply in Last Few Weeks

Source: Bloomberg

Source: Bloomberg

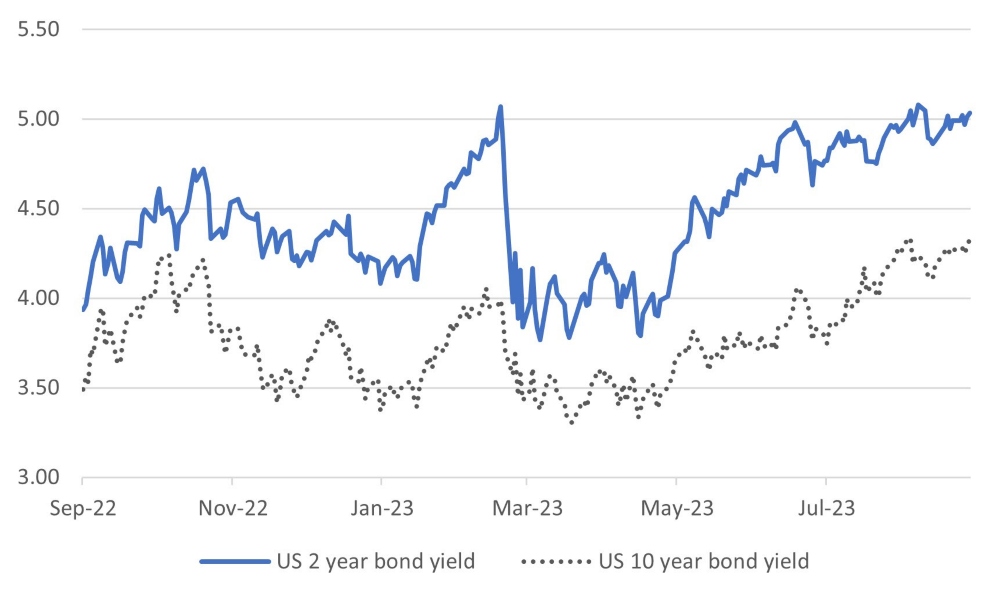

US government bond yields continue to move higher, with the 10-year bond yield reclaiming its one-year high of 4.33%. The introduction of the Fed forecasts for 2026 that are likely to show the Fed reaching their 2% inflation forecast might just help arrest the short-term increase in yields.

Chart 3: US 2-year and 10-year Government Bond Yields to Hit Short-Term Peak

Source: Bloomberg

Source: Bloomberg

Meanwhile, on 14 September, the ECB announced a further 25bps rate hike, even though parts of the eurozone economy, such as Germany, remain weak. While the ECB signalled that the rates would remain higher for longer, the market drew comfort from the message that the central bank sent out – the rate hike was in all likelihood the final in this cycle.

The persistence of inflation has kept government bond markets on the back foot. Credit remains the ongoing winner, with high-yield bonds leading the pack (global high yield +6.5% YTD). However, we expect bond markets in general to struggle in the coming quarter as they contend with the safety of 5.0-5.5% cash yields. Nevertheless, we would remind investors that cash is a one-dimensional asset, and switching the entire bond portfolio into cash is never warranted, certainly with a more medium-term view. Central bankers are fixated on bringing inflation down, even if it means pushing their respective economies into recession. To the ears of bond investors, recession risk is good news as it will likely lead to lower yields and capital gains for investors in government bonds.

China – some relief but larger worries

There was some good news from the Chinese economy last week, with a few better-than-expected economic data points helping boost hopes of a revival in sentiments. For August, retail sales (+4.6% year-on-year) and industrial production (+4.5% year-on-year) were well ahead of market expectations. Overall, China’s factory output is up at an annualised 25% rate over the three months to the end of August. Fixed asset investment of 3.2%, which is down from 3.4% for the first eight months of the year, was the only disappointing data point released last week.

Nevertheless, the improvement comes after a raft of measures announced through July and August to support the economy. Although many of these actions have been incremental in nature, a total of 44 separate measures over the past few months have certainly given the economy a sufficient nudge to put growth back on track to the aspirational 5% GDP growth level for the third quarter. On Thursday, the People's Bank of China (PBOC) provided a fresh monetary stimulus by reducing the reserve requirement ratio by 25 basis points – a measure that effectively injects 500 billion yuan ($68.7bn) of new liquidity into the system. The extra liquidity will provide some support for capital investment.

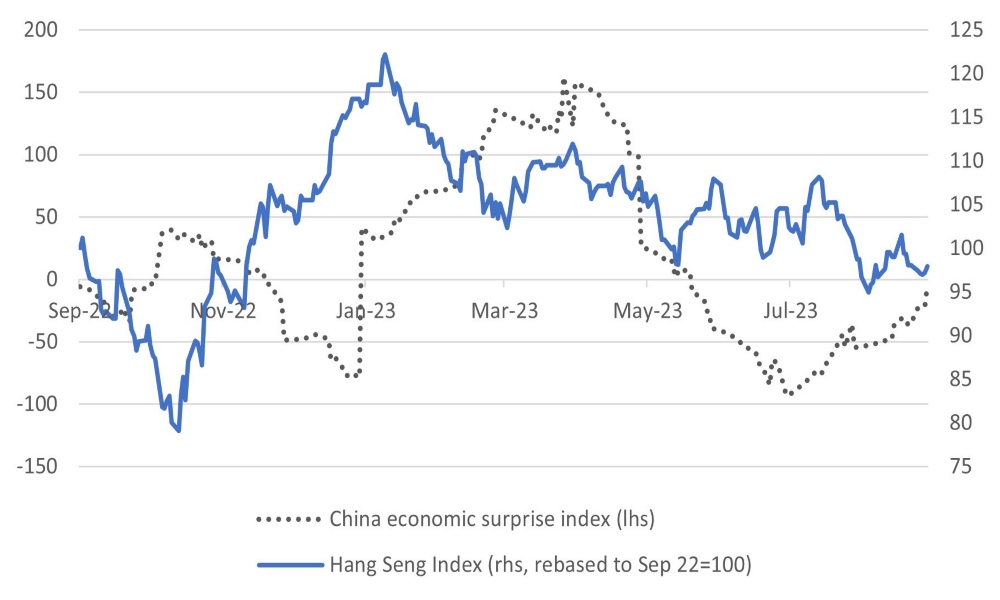

Despite the better news from China, Chinese equities drifted lower over the week after an initial knee-jerk recovery. In Hong Kong, the Hang Seng index has not shown any marked strength despite the improving economic data trends and remains 20% off its post-COVID high of January 2023. We suspect that foreign investors remain increasingly worried about the structural concerns plaguing the economy, namely the challenges in the property sector and fears of potentially less market-friendly policies from the current leadership. It was noticeable that Alibaba and JD.com, the two stocks that overseas investors have preferred previously, were down on the week. It is clear that unless an influx of domestic money happens, the market will remain depressed.

Chart 4: Improving Chinese Economic Data Has Failed to Push Hang Seng Index Higher

Source: Bloomberg

Source: Bloomberg

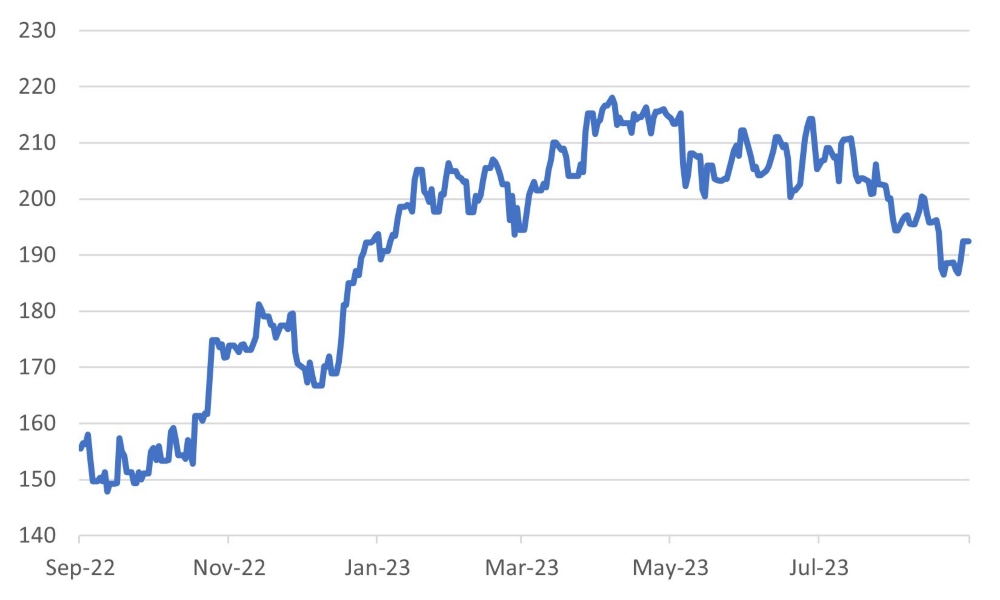

For international investors looking to buy into the Chinese recovery without buying Chinese equities, luxury goods companies (Exhibit 5) and commodity stocks are the best proxies for a recovery in Chinese demand. The only caveat on the commodity front is that the ongoing autoworkers’ strike in the US, which, if it gains momentum, could hit metal prices. This is the first time the Union of Auto Workers (UAW) has announced a strike against all the three major automakers simultaneously. The unions are asking for a 40% pay increase, with an initial 20% to be paid this year and the balance over the subsequent three-and-a-half years.

Chart 5: GS EU Luxury Goods Sector Index

Source: Bloomberg

Source: Bloomberg

Copyright © Dalma Capital, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.