The Skipping Fed

- The Fed is likely to skip this meeting and leave a rate rise for July

- Central banks of Australia and Canada both surprise the market with a policy rate rise

- ECB expected to raise rates by 25bps with an outside chance of an adjustment of policy in Japan

- Japanese equities continued to be supported by domestic positives - this past week an upward revision to 1Q growth

- Caution warranted on high yield bonds with rising defaults

The FOMC board members appear convinced about not increasing interest rates at this week’s meeting. Despite higher inflation, a tight labour market, and economic data evidencing stronger-than-expected growth, the Fed will in all likelihood maintain status quo at this week's meeting. The central bank, though, may warn that an increase in rates in July is a strong possibility. As this is an end-of-the-quarter meeting, the Fed will present its dot plots, which will likely signal that the probability of a further increase in interest rates has only grown higher. At the March meeting, the median dot for policy rates for 2023 was 5.125%. We expect the latest dot plots to show that the consensus is now for rates to peak at 5.375%, reflecting the likelihood that more Fed governors now believe that the interest rates need to rise still further. The Fed is also likely to cut its year-end unemployment rate forecast from the current 4.5% and increase its 2023 GDP forecast from the current 0.4%.

In a speech last week, vice chairman of the central bank’s board, Philip Jefferson, laid the ground for a likely skip in raising rates, arguing that “A decision to hold our policy rate constant at the coming meeting should not be interpreted to mean we have reached the peak rate of the cycle.”

The market currently prices a 31% risk of a rate hike due in part to the recent stronger-than-expected economic data and the surprises sprung by the Bank of Canada and the Reserve Bank of Australia. Last week, the Bank of Canada, which had been on hold since January, increased the overnight rate to a 22-year high of 4.75%. The market currently prices a 65% chance of another rate hike in July and has fully priced in a further tightening by September. Inflation in Canada has been stubbornly high, and the economy continues to show signs of overheating. Meanwhile, Australia's central bank also defied market expectations and increased interest rates by a quarter of a percentage point to an 11-year high and warned that it could tighten further. Many economists expect the central bank to increase interest rates by a further quarter point at its meeting in August.

The Fed also finds itself in a bit of a spot of bother since the US inflation report is due out on day one of the central bank’s two-day FOMC meeting. The consensus view is that headline inflation will fall to 4.1% from 4.9% and core inflation, too, should ease to 5.1% from 5.5%.

Across the Atlantic, there is little speculation, though, around what the ECB’s decision will be, with a 25bps rise in the reference rate widely expected by the market. Of greater interest will be the forward guidance, with a further increase in rates unlikely to be ruled out. The market currently prices a terminal rate for the current cycle of rate increases at 3.75%, which is 50bps above the current levels.

The Bank of Japan also meets this week, but is not expected to embark on a significant modification of its yield curve control (YCC) just yet. However, it is also clear that the Japanese central bank is set on a path of adjusting its monetary policy step by step. In April, the BoJ removed the interest rate guidance. We may see the central bank widen the bands or raise the targets for the YCC.

US equities need new sector leadership to make further material gains

Back in the US, a skipping Fed and growth that is holding up better than expected should help the US equity market extend its current run of positive performance. The main challenge to the market’s performance is the lack of sector rotation. The 40bps increase in the US 10-year government bond yield since early May presents a headwind to the performance of growth stocks such as technology shares, which had previously provided the lion’s share of the market’s performance. There were hopes that the energy sector would help but Saudi Arabia’s move to announce a production cut at the recently concluded OPEC meeting has not led to a sustained rally in oil prices. We note that REITs have performed better of late as they move to discount a potential peaking of the rate tightening cycle.

Table 1: S&P500 sector performances – Is the Technology sector’s leadership waning?

| % change | YTD | 1W | 1M |

| Technology | 17.1 | -0.2 | 8.1 |

| Communications | 15.3 | 1.9 | 6.1 |

| Financials | -5.1 | 2.0 | 5.4 |

| Industrials | 7.7 | 1.7 | 3.1 |

| Energy | -5.6 | 1.1 | 2.9 |

| Real Estate | 1.7 | 2.1 | 1.5 |

| Consumer Discretionary | 13.0 | 2.2 | 1.4 |

| Materials | -0.7 | 0.8 | 0.3 |

| Healthcare | -0.9 | -0.4 | -2 |

| Utilities | -3.3 | 2.2 | -2.9 |

| Consumer Staples | -1.5 | -1.0 | -4.4 |

Source: Bloomberg

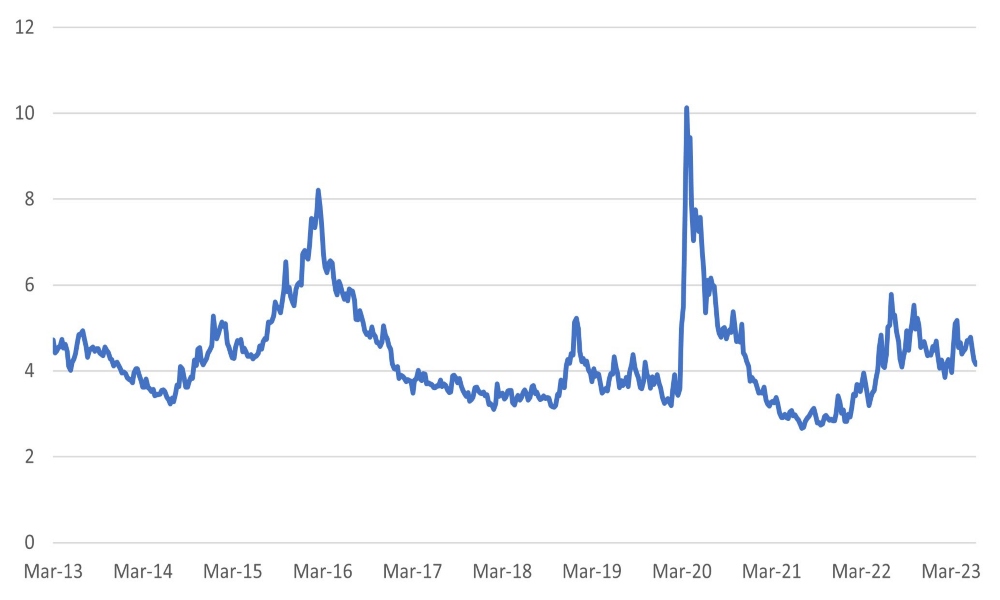

Be wary of US high yield bonds

US Bond markets have been more circumspect than equities about the prospect of monetary tightening. One asset class to be wary of is high yield bonds. Defaults have started to inch up in recent months from 1.6% at the start of the year to 2.4% through May. Despite higher defaults US high yield spreads remain relatively low at 416bps. In our view spreads could easily widen out to 500-600bps. We advocate an underweight.

Chart 1: US high yield spreads don’t look good value

Source: Bloomberg

Source: Bloomberg

Japanese equities gain support from growth - Overweight

The revisions to the first quarter GDP estimate were quite a positive surprise, with the reported 2.7% quarter-on-quarter growth compared to the initial estimate of 1.6%. The main surprise came from an upward revision to capital expenditure. Increasing to a quarter-on-quarter growth of 5.6%, up from the initial estimate of 3.8%.

China – still waiting for the magical economic stimulus – cautiously optimistic

Key data releases this week include industrial production, retail sales and fixed investment. While headline numbers for year-on-year growth may look good, the sequential monthly growth remains benign. After last week's weaker-than-expected export growth (-4.6% month-on-month), the pressure remains on the Chinese authorities to stimulate the economy. Economists expect a further cut in the reserve requirement ratio to boost lending. However, the economy wants an injection of confidence, particularly among industrialists. More monetary easing is likely to have a limited impact.

Table 2: Consensus forecasts for key Chinese economic data due this week

| Year-on-year | Month-on-month | |

| Retail sales | +13.7% | +0.2% |

| Industrial production | +3.5% | +1.5% |

| Fixed investment | +4.4% |

Source: Bloomberg

China’s equity market has drifted to close to its lows for the year in sharp contrast to the rest of the world hence we are more sanguine about being patient for performance.

Chart 2: CSI 300 Index for Chinese equities

Source: Bloomberg

Source: Bloomberg

Copyright © Dalma Capital, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.