No New Reign in Prospect for UK Asset Markets

A recent improvement in investor sentiment cannot disguise persistent structural weaknesses

- UK economy has rebounded from its winter freeze

- Structural challenges, though, leave the outlook quite uncertain

- UK is struggling to position itself as relevant in the global economy

- Interest rates have a bias to be higher than expected, which should help sterling

- UK equity market appears inexpensive – but does anyone care?

May 6th will see the crowning of King Charles III in London. Unfortunately, the coronation of a new monarch comes at a time when the asset markets in the UK are completely devoid of any crowning glory, even as they struggle to prove their relevance to international markets. Our UK-based CIO partner Bill O'Neill reflects on the developments.

Spring-time optimism after the winter freeze….

The UK economy seems to have hauled itself up quite a bit from the mid-winter despondency. The decline in energy prices and a resilient labour market have staved off the risks of a lengthy recession predicted by the Bank of England only late last year. Indeed, the latest business sentiment indicators signal momentum in growth, which is further buoyed by a robust service sector. The flash UK composite purchasing managers' index rose to 53.9 in April, up from 52.2 in March, signalling a revival in business activity. Consumer confidence looks to have turned a corner, too, with the GfK conumer confidence index rising by six points to -30 this month, beating market expectations of a reading of -35.

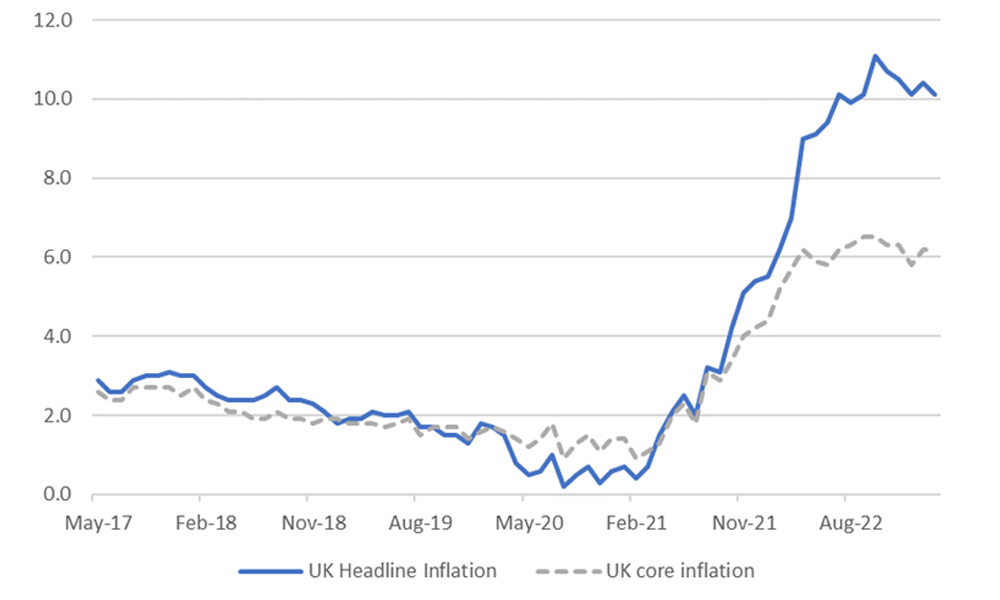

However, the story of UK consumer price inflation is much more nuanced. Unlike in other G7 economies, headline CPI inflation in the UK remains stuck at 10.1%, as of March. The inflation scenario, though, is likely to improve sharply over April and May as the base effects kick in, thanks also to the retail energy price cap. Food price inflation, too, must inevitably fall back from its current eye-watering level, although price gouging is a concern in this sector. At just above 6% per annum, UK core inflation is barely ahead of the eurozone's 5.7% and comparable with 5.6% in the US.

Chart 1: UK Headline and Core Inflation

Source: Bloomberg

…but structural obstacles to higher GDP growth and lower inflation remain embedded in the system

The broad macroeconomic outlook is still unimpressive. The Office for Budget Responsibility (OBR) in the March edition of its Outlook predicted GDP to contract 0.2% in 2023 (the weakest in G7) before growth accelerates to 1.8% in 2024. The key driver of the weakness is the slump in household real disposable and private (especially inward) investment. The Bank of England in February forecast that the level of GDP is not expected to reach the pre-COVID levels until 2026.

Nonetheless, as a likely change in government appears on the horizon, UK macroeconomic challenges increasingly focus on the weakness of its underlying growth rate both in terms of a labour market expansion and worker productivity. A myriad of factors have been quoted, such as

- A sclerotic, inconsistent planning process wedded to political interests.

- The permanently negative post-Brexit impact because of trade frictions with EU and disincentives towards inward capex.

- A regional development strategy whereby moves to decentralise economic activity might potentially enhance total factor productivity, but something that is now rapidly slipping off the government’s agenda.

- A skewed educational system not effectively aligned with an industrial strategy.

- A rising broader tax burden with the perception (at least) of increasing taxes on corporate profits. The OBR forecasts that from 2025 the government will take in about 35% of GDP in taxes, the second-highest level since the World War II.

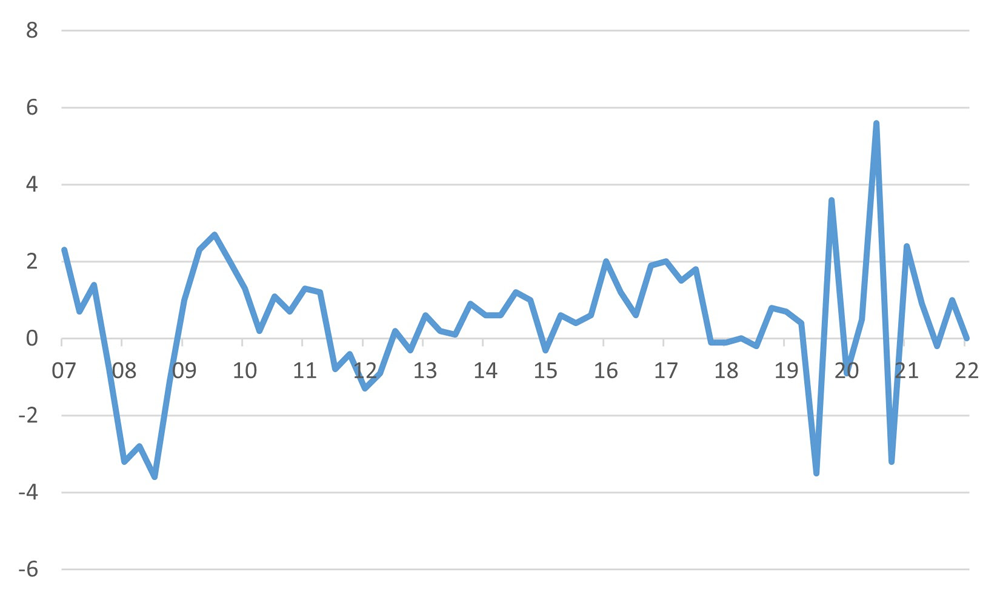

- Underlying growth in labour productivity at a paltry 0.8% p.a. accompanied by a significant shrinkage in the size of the labour force, and higher levels of inactivity post the COVID-19 pandemic.

- In sum, underlying trend growth in output continues to decline – at 1.5% today from 1.7% pre-pandemic and 2.5% pre-2008

Chart 2: Unimpressive UK Labour Productivity Growth

% change year-on-year

Source: Bloomberg

Source: Bloomberg

Result: Policymakers confronted with minimal visibility on medium-term trends

Policy makers – both on the fiscal and monetary fronts – are therefore up against an unenviable set of medium-term drivers as they look to balance support for growth with the need to bear down on core inflation over the longer term. Fiscal policy is still overshadowed by the trauma of the Liz Truss administration’s mini-budget presented last September. Market confidence has since stabilised, of course. Yet, with demography-led upward pressure on health and social spending and HM Treasury’s commitment to see the government’s debt burden decline from five years out, the scope for any fiscal support for the economy is highly limited at this juncture.

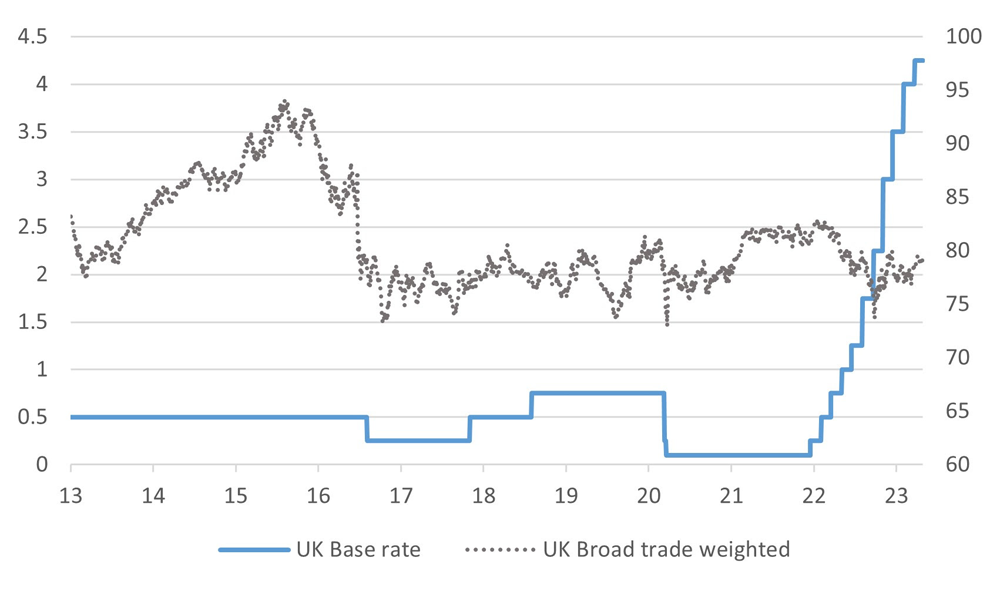

The key structural concern for the Bank of England’s Monetary Policy Committee (MPC) is the state of the labour market and, in particular, the shrinkage in supply. If inactivity persists and immigration flows become again mired in political slugfest, resulting in a persistently tight labour market, the ability of the economy to grow by even 1.5% p.a. without sparking a resulting inflation will be called into doubt.

Chart 3:

Source: Bloomberg

Most economists still expect the headline inflation rate to ease to just above 3% by December this year. The larger worry for the MPC is the challenge in forcing the underlying rate back to its targeted range of close to 2% p.a. The policy interest rate will almost certainly be hiked to 4.5% at the MPC’s May 11th meeting. The hot UK labour market, captured in an underlying growth in average earnings of 6.6% p.a., is still uncomfortably high to get close to what might be consistent with a 2% p.a. inflation over the medium term. So, it wouldn’t be a surprise if a move beyond a 5% peak in rates (as currently priced by the market at year end) isn’t soon perceived as a possibility – offering more support to a still ’cheap’ sterling over the summer months.

UK asset markets risk moving to a ‘back water’ for international investors

Investors can draw comfort from the fact that sterling in 2023 can benefit further from higher interest rates when compared to developments in other G7 economies with an easing in the pressure on household finances as energy prices decline.

Chart 4: UK 10 Year Treasury Gilt Yield vs. US Treasuries and Forward P/E of FTSE100

Source: Bloomberg

UK asset classes are at risk of becoming increasingly irrelevant to global investors. While the UK equity market includes some global brand names, it per se offers little in terms of a story. Indeed, last time the flash crash of the gilt market and a change in prime minister presented a rather unimpressive ‘story’ in UK asset markets. Nevertheless, the equity market does still offer value at a current P/E multiple that is close to the lows of the past decade. Moreover, it offers diversification versus a holding in the US equity market with a correlation of 0.56 to daily returns in USD over the past year.

Yet, the more concerning theme is international investors shying away from UK asset markets. This has been evident in the London Stock Exchange for some time with de-listings threatened and enacted – ARM being a recent example – on the premise that tighter regulations and a limited domestic investor base deter offshore companies seeking an appropriate platform for raising funds. According to the Economist, London accounted for less than 1% of the capital raised through global initial public offerings last year, compared with 18% in 2006. The UK stock market now only accounts for just 4% of the total global equity market capitalisation. The gilts market is similarly under pressure as key long-term buyers such as defined-benefit pension funds and the Bank of England go into retreat threatening to transform a ‘moron premium’ in gilt yields vs. G7 counterparts into one reflecting a fragmented buyer base.

Copyright © Dalma Capital, All rights reserved.

This document is being provided for information purposes only and on the basis that you make your own investment decisions; no action is being solicited by presenting the information contained herein. The information presented herein does not take account of your particular investment objectives or financial situation and does not constitute (and should not be construed as) a personal recommendation to buy, sell or otherwise participate in any particular investment or transaction. Nothing herein constitutes (or should be construed as) a solicitation of an offer to buy or offer, or recommendation, to acquire or dispose of any security, commodity, or investment or to engage in any other transaction, nor investment, legal, tax or accounting advice.

The information contained herein is not directed at (nor intended for distribution to or use by) any person in any jurisdiction where it is or would be contrary to applicable law or jurisdiction to access (or be distributed) and/or use such information, including (without limitation) Retail Clients (as defined in the rulebook issued from time to time by the Dubai Financial Services Authority). This document has not been reviewed or approved by any regulatory authority (including, without limitation, the Dubai Financial Services Authority) nor has any such authority passed upon or endorsed the accuracy or adequacy of this document or the merits of any investment described herein and accordingly takes no responsibility therefor.

No representation or warranty, express or implied, is made by Dalma Capital Management Limited (“Dalma”) or its affiliates as to the accuracy, completeness or fairness of the information and opinions contained in this document. Third party sources referenced are believed to be reliable but the accuracy or completeness of such information cannot be guaranteed. Neither Dalma nor any of its affiliates undertakes any obligation to update any statement herein, whether as a result of new information, future developments or otherwise.

This document contains forward-looking statements. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on current beliefs, expectations and assumptions regarding the future of the relevant business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of Dalma’s and/or its affiliates’ control. Actual results and financial conditions may differ materially from those indicated in the forward- looking statements. Forecasts are based on complex calculations and formulas that contain substantial subjectivity and no express or implied prediction made should be interpreted as investment advice. There can be no assurance that market conditions will perform according to any forecast or that any investment will achieve its objectives or that investors will receive a return of their capital. The projections or other forward-looking information regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future investment results. Past performance is not indicative of future results and nothing herein should be deemed a prediction or projection of future outcomes. Some forward looking statements and assumptions are based on analysis of data prepared by third party reports, which should be analysed on their own merits. Investments in opportunities such as those described herein entail significant risks and are suitable only to certain investors as part of an overall diversified investment strategy and only for investors who are able to withstand a total loss of investment.